Carbon Trading Systems and the Reshaping of the Construction Industry’s Future

Share:

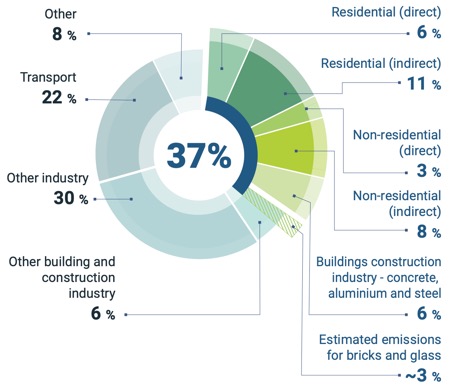

The construction industry is one of the largest sources of greenhouse gas emissions, accounting for around 37% of total global CO₂ emissions (IEA, 2022). The expansion of Emissions Trading Systems (ETS) beyond the energy sector into carbon-intensive industries — including building materials and operational processes — is reshaping the entire cost structure and competitive strategies of the construction sector.

1. Introduction

The construction industry is one of the largest sources of greenhouse gas emissions, accounting for around 37% of total global CO₂ emissions (IEA, 2022). The expansion of Emissions Trading Systems (ETS) beyond the energy sector into carbon-intensive industries — including building materials and operational processes — is reshaping the entire cost structure and competitive strategies of the construction sector.

2. ETS and the Cost of Carbon

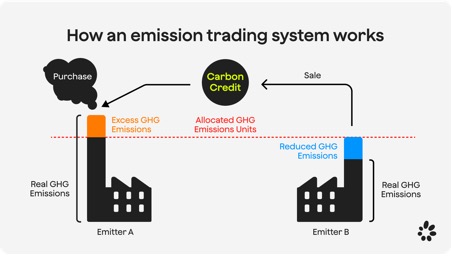

ETS establishes an emission cap and allocates allowances to companies. Those exceeding their quota must purchase additional credits, while those reducing emissions can sell their surplus.

This mechanism turns carbon into an economic cost and a tradable asset.

In the construction sector, this means that both embodied carbon (emissions embedded in materials) and operational carbon (emissions during building use) will directly influence pricing structures.

3. Impact on Building Materials

High-emission materials such as cement, steel, and glass will face significant cost pressures.

A recent study published in the Journal of Cleaner Production found that ETS implementation significantly increases the cost of carbon-intensive materials, forcing the construction sector to shift toward products with transparent Environmental Product Declarations (EPD) and lower Life Cycle Assessments (LCA).

4. Technological Innovation and Carbon Management

ETS serves as a major driver of technological innovation.

Research by ICAP (2018) demonstrates a strong correlation between ETS adoption and the rise in low-carbon technology patents.

In the construction context, this is reflected through accelerated investment in low-clinker cement, electric arc furnace (EAF) steel, material recycling, and resource-efficient design.

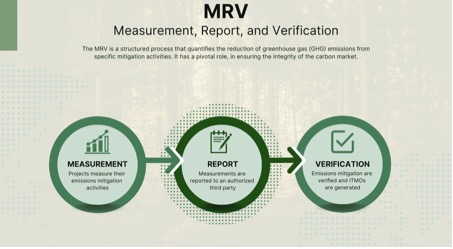

5. Data Transparency and MRV Systems

To participate in ETS, companies must implement Measurement, Reporting, and Verification (MRV) systems.

This structure closely aligns with existing green building certifications (LEED, BREEAM, LOTUS) and EPD frameworks.

Enterprises that have already adopted such systems will streamline ETS compliance while enhancing data transparency.

A study published by Springer (Li et al., 2023) emphasizes MRV as a foundational pillar for building carbon trading systems within the construction industry.

6. Linkage with Green Finance

International financial institutions such as IFC, ADB, and AIIB increasingly tie funding eligibility to emission transparency.

Thus, carbon transparency is not only a regulatory requirement under ETS but also a prerequisite for accessing green capital.

This trend strengthens the connection between carbon governance and financial competitiveness in the construction sector.

7. Outlook for Vietnam

Vietnam has begun the pilot phase of its domestic carbon market in 2025, with full operation expected by 2028 (Reuters, 2025).

The steel and cement industries will be the first to be affected, but the impacts will inevitably extend across the entire construction value chain — particularly as the EU’s Carbon Border Adjustment Mechanism (CBAM) applies to Vietnamese exports.

8. Conclusion

ETS is redefining how the construction industry operates: shifting from a cost model driven primarily by materials and labor to one shaped by carbon costs, transparent data, and low-carbon technologies.

Enterprises that proactively adopt LCA, EPD, and green certifications before ETS becomes mandatory will secure a sustainable competitive advantage — both in market positioning and financial access.

Latest news

Scope 3 Emissions - Điểm mù lớn nhất của bất động sản bền vững

Mỗi sáng, hàng nghìn người di chuyển đến tòa nhà của bạn bằng xe máy xăng, ô tô cá nhân hoặc taxi công nghệ. Mỗi chiều, họ lại rời đi theo cách tương tự. Chu trình đó lặp lại hàng trăm ngày mỗi năm - và trong suốt thời gian đó, một lượng phát thải carbon khổng lồ đang được tạo ra bên ngoài phạm vi vận hành trực tiếp của tòa nhà. Đây là “điểm mù Scope 3” của bất động sản.

ARDOR Green named Vietnam’s Top 3 LEED® Proven Providers™ by GBCI

What this means for our clients: A more efficient LEED review timeline, with approvals completed significantly faster than the standard review process. Direct and enhanced engagement with the GBCI review team, enabling complex issues to be reviewed and resolved through focused, one-on-one discussions. Independent recognition of ARDOR Green’ established expertise in LEED project administration, reflecting the firm’s high standards in design quality and documentation.

Unlocking Multi-Credit Synergies through Integrative Design in LEED v4

The realization of benefits associated with LEED starts with a transformation of the design process itself. Rather than treating credits as separate components on a checklist, an Integrative Process encourages project teams to identify synergies and interrelationships across multiple categories. By conducting early research and analysis during the "discovery" phase, teams can implement specific building features that "stack" points, achieving high levels of performance and cost-effectiveness.

Re-shaping the Construction Industry: When Emissions, Technology, and Data Become the New Market Standards

In recent years, green finance has often been cited as the key that enables Vietnamese enterprises to access international markets. However, the broader picture of the construction industry reveals a far deeper transformation: the world is not merely changing how capital is allocated, but is fundamentally restructuring the entire industry toward low emissions, advanced technology, and data transparency.

ARDOR Green Named the Only Green Design Consultancy Among Vietnam’s Sustainability Leaders

At the Vietnam Sustainable Construction Forum (VSCF) 2025, a national-level event welcoming more than 500 delegates from government agencies, businesses, industry experts, and international organizations, ARDOR Green was honored as the only design consultancy among 17 pioneering enterprises recognized for sustainable development in Vietnam’s construction industry.

Build Green, Build with ARDOR Green